कृपया इसे हिंदी में पढ़ने के लिए यहाँ क्लिक करें

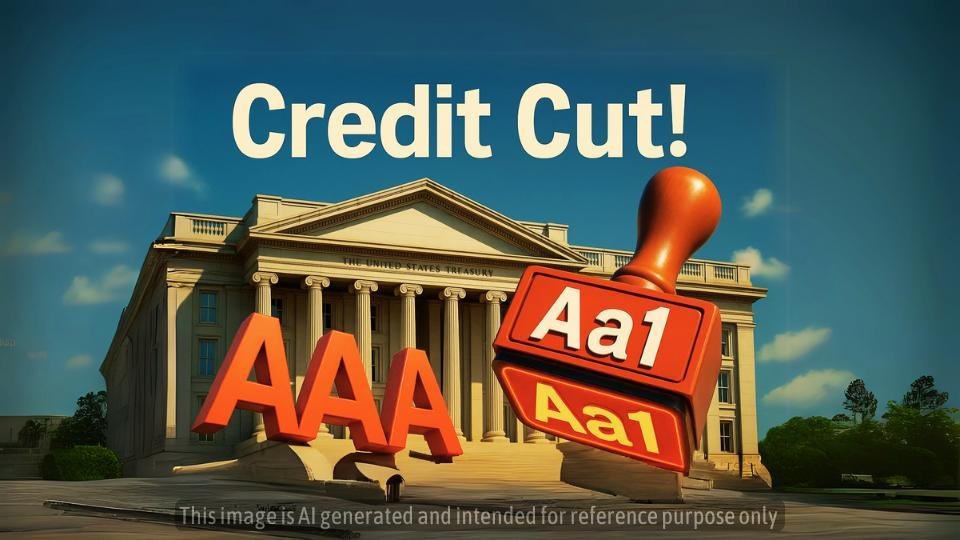

On May 16, 2025, Moody’s became the final one of the “Big Three” agencies to strip the United States of its AAA status, downgrading its long-term sovereign rating from Aaa to Aa1 (the equivalent of AA+) due to rising debt and persistent fiscal deficits. This follows Standard & Poor’s downgrade in August 2011 and Fitch’s move in August 2023, meaning no major agency now views U.S. debt as top-tier. The downgrade may raise borrowing costs, compound market jitters, and shape the political narrative around President Trump’s economic agenda, including his push to extend the 2017 Tax Cuts and Jobs Act.

Backstory: How We Got Here

2011: S&P’s First Cut

- On August 5, 2011, S&P cut the U.S. rating from AAA to AA+, citing political brinkmanship over the debt ceiling and doubts about policymaking stability.

- The so-called “Debt-Ceiling Crisis” saw Congress debating whether to raise the borrowing limit, spooking global investors.

2020–2023: Warning Signs and Fitch’s Warning

- In July 2020, Fitch placed the AAA rating on Negative Outlook, warning that U.S. debt would exceed 130% of GDP by 2021 amid COVID-19 spending.

- On May 24, 2023, Fitch officially put AAA on Rating Watch Negative during another debt-ceiling standoff.

- Finally, on August 1, 2023, Fitch downgraded to AA+, citing large deficits and lack of a credible fiscal plan.

The May 16, 2025 Moody’s Downgrade

- Moody’s announced the cut from Aaa to Aa1, pointing to a $36 trillion national debt, growing interest costs, and a series of fiscal impasses in Washington.

- Despite the downgrade, Moody’s assigned a Stable Outlook, acknowledging the U.S. economy’s size, resilience, and the dollar’s reserve-currency role.

What This Means for Trump

Political Narrative

- President Trump and his team argue the downgrade stems from “Biden-Era spending” and Democratic gridlock, framing it as evidence of liberal fiscal mismanagement.

- Democrats counter that prior cuts—especially the 2017 Tax Cuts and Jobs Act championed by Trump—widened deficits and left little room for new emergencies.

Campaign Implications

- Higher borrowing costs could complicate any second-term agenda, making it harder to finance promises like further tax cuts or large infrastructure bills.

- Analysts warn Treasury yields may tick upward, affecting mortgage rates, student loans, and corporate borrowing.

Economic Impact: From Wall Street to Main Street

Borrowing Costs

- Markets reacted with a modest rise in 10-year Treasury yields as investors demanded a higher premium for perceived risk.

- Mortgage rates could climb by 0.1–0.2 percentage points, translating to hundreds of dollars extra per month for homeowners.

Global Sentiment

- Rival economies (e.g., Germany, Japan) may see a slight uptick in demand for their bonds as investors seek top-tier safety.

- Some emerging-market investors worry about a stronger dollar, which raises the cost of servicing dollar-denominated debt.

Little-Known Facts & Surprising Details

- Unknown to many, the U.S. Treasury had prepared “contingency payment plans” in case of a default scenario, choosing which obligations to pay first.

- The Federal Reserve has advised banks to run stress tests assuming rates as high as 5.5%, ensuring resilience if yields spike further.

Conclusion

The loss of the ultimate AAA badge underscores long-standing concerns over U.S. fiscal health. For President Trump, it offers both a campaign talking point and a real policy challenge: balancing popular tax cuts with sustainable debt levels. As markets and Main Street adjust, every household may feel the ripple effects—making fiscal discipline a topic even at the local bake sale.

Leave a Reply